When a business owner divorces in Illinois, the collaborative process replaces costly dueling expert valuations and court-imposed outcomes with a single neutral business valuation professional, private negotiations, and a Marital Settlement Agreement both spouses helped build — protecting the business, its employees, and both parties’ financial futures.

Anna P. Krolikowska, J.D., Former ISBA President and Super Lawyer 2019–2025 at Anna K Law, a Northbrook, Illinois family law firm, guides business-owning couples through Illinois divorce with a coordinated team of attorneys, a financial neutral, and a certified business valuation expert — focused on one outcome: a workable agreement, not a courtroom ruling.

Key Takeaways:

- A marital interest in a business is the portion of the business’s value accumulated during the marriage, subject to equitable division under the Illinois Marriage and Dissolution of Marriage Act (750 ILCS 5/503)

- Illinois excludes personal goodwill from marital assets — only enterprise goodwill is subject to division.

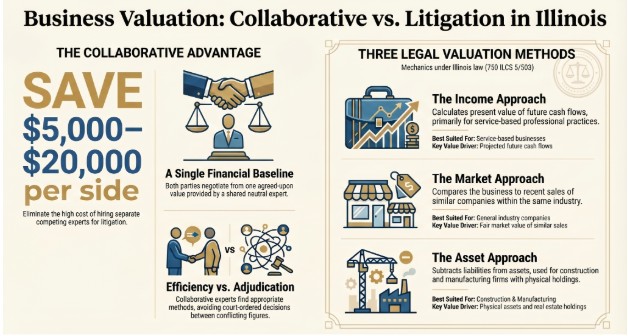

- Business valuations in litigated Illinois divorces cost $5,000–$20,000 per side; collaborative divorce uses one shared neutral valuator.

- The collaborative process produces six resolution paths that courts cannot custom-build without full litigation.

Why Does Business Ownership Make Illinois Divorce More Complicated?

Business ownership complicates an Illinois divorce because a privately held company must be classified, valued, and divided under 750 ILCS 5/503—a process requiring financial expertise, legal precision, and operational decisions that standard divorce agreements were never designed to handle.

A privately held business — whether structured as a sole proprietorship, LLC, S-corporation, or professional practice — carries tangible assets, intangible assets, goodwill, retained earnings, and future income projections that require a certified business valuation professional to assess accurately.

Illinois courts require fair market value determinations under the Illinois Marriage and Dissolution of Marriage Act (750 ILCS 5/503), and competing expert valuations between spouses routinely produce figures that diverge by hundreds of thousands of dollars.

Business ownership in divorce also raises questions no property spreadsheet resolves: Does the non-owner spouse hold a marital interest based on indirect contributions—managing the household while the other built the company?

Did the business-owning spouse withhold retained earnings to suppress apparent value? Who manages the company while divorce proceedings remain active? Resolving those questions requires a coordinated professional team, not a contested courtroom hearing.

Illinois business owners evaluating their divorce options can use the collaborative process to address every dimension — legal, financial, operational, and personal — through a single structured process outside of court.

Own a business and facing divorce in Illinois? Anna P. Krolikowska coordinates attorneys, financial neutrals, and valuation experts to protect your business through the collaborative process. Schedule a Consultation at Anna K Law

What Is the Difference Between Marital and Non-Marital Business Interests in Illinois?

The marital vs. non-marital classification of a business interest determines which portion of the company’s value is subject to equitable division — and misclassifying that boundary is one of the most financially consequential errors an Illinois business owner can make in a divorce.

A marital interest in a business is the portion of the business’s value accumulated during the marriage, subject to equitable division under 750 ILCS 5/503.

A non-marital interest is the portion tied to pre-marital ownership, inheritance, or gift, and the appreciation of non-marital property is also generally non-marital under Illinois case law established in In re Marriage of Kennedy, 418 NE 2d 947 (Ill. App. 1981).

| Factor | Marital Implication |

| Business started during marriage | Presumed marital property under 750 ILCS 5/503 |

| Business started before marriage, grew during marriage | Pre-marital portion non-marital; growth may be marital if marital funds or effort contributed |

| Non-owner spouse contributed time, labor, or indirect support | May create marital interest in a pre-marital business |

| Business purchased with pre-marital assets | May retain a non-marital character despite marriage timing |

| Personal goodwill of the owner | Non-marital under Illinois Supreme Court precedent; excluded from division |

Illinois law distinguishes enterprise goodwill — the business’s institutional reputation, client base, and transferable value — from personal goodwill — the owner’s individual reputation and relationships that would not survive a change in ownership.

Only enterprise goodwill qualifies as a marital asset subject to equitable division. This distinction, rooted in Illinois Supreme Court precedent, can substantially reduce the taxable marital value of a professional practice.

In a collaborative divorce, the financial neutral and the business valuation professional trace these classifications jointly — so the marital interest is calculated accurately before any negotiation begins.

The Anna K Law equitable vs. equal distribution guide explains how Illinois courts apply these classifications in property division proceedings.

What Business Valuation Options Do You Have in a Collaborative Divorce?

Collaborative divorce gives both spouses access to a single shared neutral business valuation professional — eliminating the $5,000–$20,000 per-side cost of dueling litigation experts and producing a single agreed-upon value both parties can negotiate from.

Illinois courts recognize three primary valuation methods under the equitable distribution standards of 750 ILCS 5/503:

Income Approach

The income approach calculates the present value of projected future cash flows, discounted at an appropriate capitalization rate. Illinois courts most frequently apply this method to service-based businesses and professional practices, where future earnings constitute the primary value driver.

Market Approach

The market approach compares the business to recent sales of similar companies in the same industry, size range, and geographic market. This method produces a fair market value that reflects what a willing buyer would pay a willing seller — the evidentiary standard that Illinois courts apply under established case law.

Asset Approach

The asset approach subtracts total liabilities from total business assets. This method applies most accurately to asset-heavy businesses — construction companies, manufacturing operations, and real estate holding entities — where physical assets drive value more than income projections.

In a litigated Illinois divorce, each spouse retains a separate valuation expert who applies different methods and different assumptions — forcing a court to adjudicate between competing figures at additional cost.

In a collaborative divorce, one shared neutral valuator applies the most appropriate method for the specific business type, so both spouses negotiate from the same financial baseline. The Anna K Law asset division guide covers how the financial neutral applies valuation results to build resolution options.

What Are the Six Ways Illinois Couples Resolve Business Ownership in Collaborative Divorce?

Illinois collaborative divorce offers six structured resolution paths for business ownership — each designed to preserve operational continuity, protect both spouses’ financial interests, and avoid a court-imposed forced sale.

1. Buyout with Offsetting Marital Assets

The business-owning spouse retains full ownership. The non-owning spouse receives marital assets of equivalent value — the family home, retirement accounts, investment portfolios, or cash — so no money changes hands directly for the business. This path works when the marital estate contains sufficient non-business assets to offset the business’s marital value.

2. Structured Cash Payments Over Time

The business-owning spouse purchases the other spouse’s marital interest through installment payments over an agreed period — typically two to five years. The Marital Settlement Agreement specifies the payment schedule, interest rate, and security provisions.

This path works when the marital estate lacks sufficient liquid assets for an immediate offset, but the business generates consistent monthly income.

3. Co-Ownership with a Post-Divorce Operating Agreement

Both spouses retain ownership and continue operating the business under a formal post-divorce operating agreement that defines roles, compensation, profit distribution, and exit terms.

This path requires a professional relationship that both parties can sustain and works best when both spouses hold skills the business genuinely needs.

4. Transitional Consultant Arrangement

The departing spouse relinquishes ownership but remains engaged as a paid consultant for a defined period—typically six to eighteen months. This path protects client relationships and institutional knowledge while providing income to the departing spouse during the transition. The arrangement terminates on a fixed schedule with no ongoing ownership tie.

5. Third-Party Sale of One Spouse’s Interest

The departing spouse sells their ownership interest to an existing business partner, qualified investor, or approved third party. The departing spouse receives sale proceeds; the remaining spouse gains a new business partner rather than a buyout obligation. This path works when the business’s existing operating agreement permits ownership transfers.

6. Joint Sale with Division of Proceeds

Both spouses sell the business to a third-party buyer and divide net proceeds according to their negotiated marital interest percentages.

This path delivers a clean financial separation and eliminates all ongoing business entanglement — and works best when neither spouse wishes to continue operating the business or when a buyout is financially infeasible.

Collaborative divorce produces all six paths through private negotiation guided by the collaborative divorce team at Anna K Law. Litigation produces one outcome: a court-imposed order that the judge determines is equitable, without the operational flexibility or timeline sensitivity a business requires.

What Is the Emotional Weight of a Business in Divorce — and How Does Collaborative Divorce Address It?

A privately held business represents more than a marital asset — it carries the owner’s professional identity, employee relationships, family legacy, and years of personal sacrifice, and the collaborative process is the only Illinois divorce framework that explicitly addresses those dimensions alongside the legal and financial ones.

For many Illinois business owners, the company embodies decisions made across an entire career — the owner’s name, long-term client relationships, and employees whose livelihoods depend on the business remaining stable.

Losing control through a court-imposed order produces a category of financial and personal loss that property division formulas cannot measure.

A collaborative financial neutral is a Certified Divorce Financial Analyst who models financial outcomes and facilitates structured conversations about what the business means to each spouse — not just its value.

That professional creates space for both parties to articulate priorities before any resolution path is selected, so you can reach an agreement built around your actual goals.

The non-owning spouse carries equivalent weight. A spouse who managed the household while the other built the company contributed to that business’s success in ways balance sheets do not record.

The collaborative process gives that contribution explicit recognition in the negotiation, rather than reducing it to a line in a court order.

Illinois business owners who want agreements both parties will follow — rather than orders both parties will resent — can explore the collaborative approach at Anna K Law.

A business you built deserves a divorce process that protects it. Anna K Law keeps valuation, division, and operational decisions out of a courtroom and in your hands. Explore Your Options with Attorney Krolikowska

What Happens to Your Business If You Choose Litigation Over Collaboration?

Litigating a business-ownership divorce in Illinois exposes the company to mandatory public financial disclosure, competing expert valuations, court-imposed division outcomes, and operational disruption that continues for the full duration of proceedings — with a final order neither spouse designed and both must implement.

A litigated Illinois divorce involving a business triggers mandatory financial discovery. Tax returns, profit-and-loss statements, shareholder agreements, payroll records, and client lists become part of the public court record — accessible to employees, competitors, clients, and lenders.

For a privately held business whose value depends on reputation and client confidence, that disclosure produces operational damage no court order can reverse.

Illinois litigated divorce proceedings involving business assets routinely produce four compounding problems:

- Competing expert valuations that diverge by $100,000 or more, with additional court costs required to resolve the gap

- Temporary relief orders under 750 ILCS 5/501 restricting one spouse from business operations during proceedings — potentially removing the operating spouse from management mid-case

- A forced buyout at a court-determined value, neither spouse negotiated nor agreed to

- A resolution timeline measured in months or years, rather than the weeks, a collaborative process requires

The Illinois Collaborative Process Act (2017) requires all financial disclosures to remain confidential between the parties and their professional team. The business’s value, structure, and resolution path never enter the public record.

The Marital Settlement Agreement is entered by the court as a fully agreed order, not imposed after contested proceedings.

An average contested Illinois divorce costs $15,000–$30,000 per spouse in attorney fees alone — before business valuation costs of $5,000–$20,000 per side, forensic accountant fees, and multiple court hearings are added.

For business owners evaluating the long-term financial implications of divorce, the cost differential between collaborative and litigated resolution is not marginal.

The IRS Publication 504 outlines the federal tax treatment of asset transfers incident to divorce — a dimension the collaborative financial neutral addresses directly within the settlement structure.

Frequently Asked Questions

What makes business ownership more complicated in an Illinois divorce?

Business ownership requires classification as marital or non-marital property, a certified fair market valuation, and a negotiated resolution for the business’s operational future — all governed by 750 ILCS 5/503. These demands exceed what standard divorce agreements address and require financial and legal professionals with business-specific expertise.

What is a marital interest in a business under Illinois law?

A marital interest in a business is the portion of the business’s value accumulated during the marriage, subject to equitable division under the Illinois Marriage and Dissolution of Marriage Act (750 ILCS 5/503). Pre-marital ownership and the appreciation of pre-marital business value are generally non-marital under Illinois case law.

Is personal goodwill a marital asset in Illinois?

No. Illinois courts exclude personal goodwill — the owner’s individual reputation, client relationships, and professional skills — from marital assets subject to division. Only enterprise goodwill, the business’s institutional value and transferable client base, qualifies as a divisible marital asset. This exclusion can substantially reduce the marital value of a professional practice or service business.

How much does a business valuation cost in an Illinois divorce?

In a litigated Illinois divorce, each spouse retains a separate business valuation expert at a cost of $5,000–$20,000 per side, depending on the business’s complexity and the required valuation method. Collaborative divorce uses one shared neutral business valuation professional — a single cost divided between both parties, with no competing expert testimony to adjudicate.

What are the six resolution paths for a business in a collaborative divorce?

Illinois collaborative divorce produces six resolution paths: (1) buyout with offsetting marital assets, (2) structured cash payments over time, (3) post-divorce co-ownership with a formal operating agreement, (4) transitional consultant arrangement, (5) third-party sale of one spouse’s ownership interest, and (6) joint sale with negotiated division of proceeds. Litigation produces one outcome — a court-imposed order.

Can a non-owning spouse claim a marital interest in a business started before marriage?

Yes. A non-owning spouse who contributed to the business’s growth during the marriage — through direct labor, financial support, or indirect contributions such as managing the household — may hold a marital interest in the appreciation of a pre-marital business under Illinois equitable distribution law.

How does collaborative divorce protect business confidentiality?

The Illinois Collaborative Process Act (2017) restricts all financial disclosures to the parties and their professional team. Business financials, valuation reports, and resolution terms do not enter the public court record. Litigated divorce converts those same documents into discoverable, publicly accessible court filings.

What is the difference between enterprise goodwill and personal goodwill in Illinois?

Enterprise goodwill is the business’s transferable institutional value — brand recognition, client base, and operational systems that survive a change in ownership. Personal goodwill is the non-transferable value tied to the individual owner’s reputation and relationships. Illinois courts include enterprise goodwill in marital assets and exclude personal goodwill from equitable division.

How long does a collaborative divorce involving a business take in Illinois?

A collaborative divorce involving a business resolves more quickly than a litigated case because both parties work from a single, shared valuation and negotiate directly with professional guidance. Collaborative cases avoid the scheduling delays, motion practice, and court calendar backlogs that extend litigated business divorces by months or years.

Where can I get legal guidance on divorcing as a business owner in Illinois?

Anna P. Krolikowska, J.D., at Anna K Law, a Northbrook, Illinois family law firm, offers consultations for Illinois business owners navigating divorce. Attorney Krolikowska is a Former ISBA President, Super Lawyer 2019–2025, ABA Commission on Women in the Profession Commissioner (2023–2026), Trained Mediator, and Collaborative Practitioner.

Anna K Law coordinates attorneys, financial neutrals, and business valuation professionals into one private, structured process — so your company emerges from divorce intact. Book Your Consultation with Anna K Law →

Anna P. Krolikowska, an attorney in the Northbrook law firm of Anna P. Krolikowska P.C, focuses her practice in the area of family law. Anna realizes that importance and the impact family law matters have not only on her clients, but also on their families. From divorce and child custody to any judgment modifications, Anna considers the unique circumstances of each case to develop a course of action designed specifically to address each client’s unique needs.