Gray divorce — defined as divorce among spouses age 50 and older — carries financial consequences that standard divorce agreements are not built to handle. Retirement assets, health insurance continuity, spousal maintenance duration, and a compressed timeline to rebuild savings make every decision in an Illinois gray divorce consequential in ways that a younger couple’s divorce is not.

As of 2026, Pew Research Center data show that gray divorce has risen from 8% of all U.S. divorces in 1990 to more than one-third today. Research from Bowling Green State University’s National Center for Family and Marriage Research found that women over 50 face a 45% decline in standard of living post-divorce compared to a 21% decline for men — a 24-percentage-point gap that persists across income levels and education backgrounds.

Anna P. Krolikowska, J.D., Former ISBA President and Super Lawyer 2019–2025 at Anna K Law, a Northbrook, Illinois family law firm, guides spouses over 50 through Illinois divorce with a collaborative team that includes a Certified Divorce Financial Analyst and retirement planning expertise — so every financial decision is modeled before it is finalized.

Key Takeaways:

- A QDRO is a Qualified Domestic Relations Order — a court order that divides a retirement plan between divorcing spouses without triggering early withdrawal penalties or immediate taxation under IRS retirement plan division rules.

- Illinois spousal maintenance for marriages of 20 years or longer may be awarded indefinitely under 750 ILCS 5/504

- Federal COBRA covers health insurance continuation for up to 36 months post-divorce — but spouses between 50 and 65 face a coverage gap before Medicare eligibility that COBRA alone does not close.

- Spousal maintenance awarded on or after January 1, 2019, is tax-neutral — not deductible for the payer and not taxable income for the recipient under current IRS Publication 504 rules.

- The Illinois Spousal Continuation Coverage Law (215 ILCS) extends health coverage beyond COBRA for qualifying spouses, regardless of employer size.

What Makes Gray Divorce Financially Different From Divorce at Younger Ages?

Gray divorce is financially distinct because spouses over 50 carry fewer remaining working years to rebuild divided assets, hold larger and more complex retirement portfolios requiring QDRO division, face health insurance gaps spanning up to 15 years before Medicare eligibility, and qualify for longer spousal maintenance durations — making every Illinois settlement decision more financially consequential than in a younger divorce.

A couple divorcing at 35 has 25–30 years to rebuild savings after asset division. A couple divorcing at 55 retains a decade or less.

That compressed recovery window changes the relative stakes of every settlement decision — which retirement account each spouse retains, how spousal maintenance is structured, whether the family home is sold or retained, and how health coverage is secured between the divorce date and Medicare eligibility at age 65.

Illinois gray divorce carries a specific maintenance exposure. Under 750 ILCS 5/504, marriages of 20 years or longer qualify for indefinite maintenance — meaning the paying spouse may carry that monthly obligation for the remainder of their working life.

A collaborative financial neutral evaluates every proposed settlement path before the Marital Settlement Agreement is signed — so you can evaluate each option against its true long-term cost, not just its face value.

Illinois spouses over 50 evaluating their divorce options can use the collaborative process to access the financial modeling, privacy protection, and professional expertise that gray divorce specifically requires.

What Are the Two Gray Divorce Financial Profiles Illinois Couples Face?

Illinois gray divorce couples fall into two profiles — dual-income households and one-income households — each carrying opposite financial risks that require opposite planning strategies, because conflating the two produces settlements that financially fail one spouse within five years of signing.

Dual-Income Households

Both spouses carry individual 401(k) plans, retirement accounts, and separate Social Security earnings histories built over 20–30 working years. The primary financial risk in dual-income gray divorce is the complexity of asset division — each spouse holds retirement portfolios with pre- and post-marital portions that require precise tracing before any QDRO is drafted.

The secondary risk is maintenance miscalculation. Illinois guideline maintenance applies when the combined gross annual income falls below $500,000. When both spouses earn comparable incomes, maintenance may be minimal or absent.

Where income diverges significantly, the higher earner may owe maintenance for a duration calculated as a substantial multiplier of the marriage length under 750 ILCS 5/504(b-1).

One-Income Households

The earning spouse holds all retirement assets and employer-sponsored health insurance and is the primary source of income.

The non-earning spouse — typically the spouse who reduced workforce participation to support the family — faces three simultaneous financial gaps post-divorce: retirement savings substantially below the earning spouse’s balance, an immediate loss of employer-sponsored health coverage, and dependence on spousal maintenance as the primary source of income.

The Illinois spousal maintenance formula under 750 ILCS 5/504 calculates the monthly award as 33.3% of the payer’s net income minus 25% of the recipient’s net income, capped at 40% of the combined net income.

A collaborative financial neutral model considers both household profiles before any settlement is proposed, so the agreement reflects the actual post-divorce financial reality that both spouses will live in.

The Anna K Law long-term financial implications guide details how these decisions compound over a 20-year retirement horizon.

Facing a gray divorce in Illinois and uncertain about your retirement and maintenance picture? Anna P. Krolikowska will model every financial scenario before you sign anything. Schedule Your Consultation

What Happens to 401(k)s, Pensions, and QDROs in an Illinois Gray Divorce?

A QDRO divides a 401(k) or pension between divorcing spouses without triggering early withdrawal penalties or immediate taxation — but each order must be drafted correctly, submitted to the plan administrator before the divorce is finalized, and structured as a separate instrument for each retirement account — so you protect the full after-tax value of every asset being divided.

A Qualified Domestic Relations Order is a court order that instructs a retirement plan administrator to divide plan assets between a plan participant and an alternate payee — typically a divorcing spouse — without triggering the 10% early withdrawal penalty that applies to distributions before age 59½.

The IRS defines a QDRO as a judgment, decree, or order requiring a retirement plan to pay marital property rights to a spouse or former spouse.

| Retirement Account Type | QDRO Required | Key Rule |

| 401(k), 403(b), 457(b) | Yes | Division tax-free at time of QDRO; ordinary income tax applies on future distributions |

| Defined benefit pension | Yes (QILDRO for Illinois government pensions) | No payout until plan participant retires; actuarial calculation required |

| IRA / Roth IRA | No | Divided by divorce decree as transfer incident to divorce — no QDRO required |

Illinois law under 750 ILCS 5/503(b)(2) presumes all retirement benefits accumulated during the marriage to be marital property subject to equitable division.

Pre-marital account balances are non-marital and excluded from division — but tracing that boundary requires financial documentation spanning 20 to 30 years in a long-term marriage.

One QDRO option frequently overlooked in gray divorce is the immediate cash distribution.

A spouse who receives a QDRO distribution from a 401(k) can take an immediate cash distribution — without incurring the 10% early withdrawal penalty — even if the receiving spouse is under age 59½. Federal income tax applies to the distributed amount.

This penalty waiver is available only at the time of the initial QDRO distribution and does not apply to IRA divisions.

What Is the Health Insurance Gap in Gray Divorce — and How Do Illinois Spouses Close It?

The health insurance gap in gray divorce is the uninsured window between the divorce finalization date and Medicare eligibility at age 65 — a gap spanning 10 to 15 years for spouses divorcing in their early 50s that federal COBRA’s 36-month maximum coverage cannot bridge alone.

A spouse covered under the other spouse’s employer health plan loses that coverage when the Illinois divorce is finalized.

Three continuation coverage options exist, each with distinct cost structures, duration limits, and employer size requirements:

| Coverage Option | Duration | Employer Size Requirement | Key Cost |

| Federal COBRA | Up to 36 months | 20+ employees | Up to 102% of full premium — no employer subsidy |

| Illinois Spousal Continuation Coverage (215 ILCS) | Until Medicare eligibility for spouses 55+; 2 years for spouses under 55 | All Illinois fully insured group plans, regardless of size | Full premium — no employer subsidy |

| ACA Marketplace Plan | Ongoing; annual renewal | None | Premium tax credits are available to individuals below 400% of the federal poverty level |

The Illinois Spousal Continuation Coverage Law (215 ILCS) extends health coverage beyond federal COBRA in two ways that directly protect gray divorce spouses: the law applies to all Illinois fully insured group health plans regardless of employer size, and it provides coverage until Medicare eligibility for spouses age 55 or older at the time of the qualifying event.

The departing spouse must notify the employer and insurer in writing within 30 days of the divorce to activate this right.

Federal COBRA applies only to employers with 20 or more employees and provides continuation for up to 36 months at a cost of up to 102% of the full premium.

A spouse who divorces at age 52 and exhausts COBRA’s full 36-month period reaches age 55 still uninsured, 10 years before Medicare eligibility. Illinois Spousal Continuation Coverage closes that gap for spouses who qualify by age.

A collaborative divorce agreement structures maintenance payments to fund the departing spouse’s health insurance premiums directly, so the annual premium cost is addressed inside the settlement rather than surfacing as an unfunded obligation after it is signed.

How Does a Collaborative Financial Neutral Change the Planning Equation in Gray Divorce?

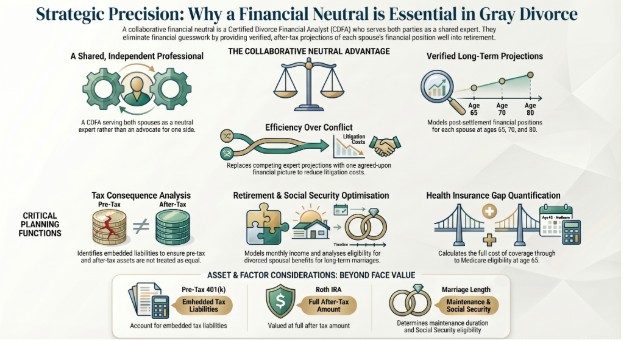

A collaborative financial neutral eliminates financial guesswork in gray divorce by modeling the after-tax, post-maintenance, post-QDRO financial position of both spouses under every proposed settlement — so neither spouse signs a Marital Settlement Agreement without a verified projection of their financial position at age 65, 70, and 80.

A collaborative financial neutral is a Certified Divorce Financial Analyst (CDFA) who serves both spouses as a shared neutral professional — not an advocate for either party.

In a gray divorce, the collaborative financial neutral performs five planning functions that neither collaborative attorney is trained to replicate:

- Retirement income projection: Models each spouse’s projected monthly income from Social Security, 401(k) accounts, and any pension at retirement age — so the settlement reflects post-retirement income, not just current account balances

- Tax consequence analysis: Identifies embedded tax liabilities in each asset category — pre-tax 401(k) vs. Roth IRA vs. after-tax brokerage — so a $200,000 pre-tax account is not treated as equivalent in value to a $200,000 Roth account

- Maintenance modeling: Calculates the long-term cost and duration of spousal maintenance under 750 ILCS 5/504 across multiple marriage-length scenarios — including indefinite maintenance exposure for 20-year marriages

- Health insurance gap quantification: Calculates the full premium cost of COBRA and Illinois Spousal Continuation Coverage through Medicare eligibility at age 65 and incorporates that figure into the maintenance or asset offset calculation

- Social Security optimization: Analyzes whether the lower-earning spouse qualifies for divorced spousal Social Security benefits based on the higher earner’s record — a federal benefit available to divorced spouses married at least 10 years, equal to up to 50% of the higher earner’s primary insurance amount

In a litigated gray divorce, each spouse retains a separate financial expert — producing competing projections that a judge must adjudicate between.

In a collaborative divorce, one shared neutral financial professional produces a single agreed-upon financial picture that both spouses negotiate from — eliminating duplication costs and competing assumptions simultaneously.

What Asset Protection Strategies Does the Collaborative Process Make Available for Gray Divorce?

The collaborative process makes five asset protection strategies available to Illinois gray divorce spouses that litigated divorce cannot replicate — because each strategy requires mutual agreement, coordinated financial modeling, and professional implementation, which a contested courtroom timeline structurally precludes.

1. Pre-Tax vs. After-Tax Asset Equalization

The collaborative financial neutral calculates the after-tax value of every retirement and investment account before any division is proposed. A pre-tax 401(k) carries a future ordinary income tax liability that a Roth IRA does not carry.

Equalization based on nominal account balance rather than after-tax value systematically disadvantages the spouse who receives the pre-tax assets — a structural error the collaborative process corrects before the agreement is drafted.

2. Defined Benefit Pension Offset

Rather than dividing a pension through a QDRO — which requires actuarial calculation and delays payout until the plan participant retires — both spouses can negotiate a pension offset.

The pension-holding spouse retains the full pension benefit. The other spouse receives a larger share of the other marital assets of equivalent present value. This eliminates QDRO complexity and removes the years-long wait for pension distributions to begin.

3. Structured Maintenance with Health Insurance Allocation

Collaborative divorce allows both spouses to structure spousal maintenance to include a specific dollar allocation for health insurance premiums — so the departing spouse’s COBRA or Illinois Spousal Continuation Coverage cost is funded explicitly within the maintenance order rather than absorbed as an unplanned expense out of general maintenance income.

4. Social Security Timing Coordination

A divorced spouse married at least 10 years qualifies for Social Security spousal benefits equal to up to 50% of the higher earner’s primary insurance amount — without reducing the higher earner’s own benefit.

The collaborative financial neutral models the optimal claiming age for each spouse to maximize total lifetime Social Security income — a calculation that changes materially depending on whether one spouse claims at 62, 67, or 70.

5. Lump-Sum Maintenance Buyout

Rather than carrying an indefinite monthly maintenance obligation, both spouses can negotiate a lump-sum maintenance settlement — a single payment that terminates the maintenance relationship entirely and eliminates the risk of modification.

The collaborative financial neutral calculates the present value of the projected maintenance stream so both spouses evaluate the lump sum against a verified actuarial baseline rather than an estimate.

None of these five strategies is available by court order without mutual agreement. All five require coordinated financial and legal planning that the collaborative divorce process at Anna K Law is specifically structured to deliver.

The financial decisions made in a gray divorce shape your retirement for decades. Anna K Law’s collaborative team — attorneys, Certified Divorce Financial Analyst, and retirement planning expertise — models every outcome before you commit. Start Your Consultation

Frequently Asked Questions

What makes gray divorce financially different from divorce at younger ages?

Gray divorce is financially different because spouses over 50 carry larger retirement portfolios requiring QDRO division, face health insurance gaps of up to 15 years before Medicare eligibility at 65, qualify for longer maintenance durations under 750 ILCS 5/504, and retain fewer working years to rebuild divided assets — making every Illinois settlement decision structurally more consequential than in a younger divorce.

What is a QDRO in an Illinois divorce?

A QDRO is a Qualified Domestic Relations Order — a court order that divides a 401(k), pension, or other qualified retirement plan between divorcing spouses without triggering the 10% early withdrawal penalty or immediate taxation. Illinois law requires a separate QDRO for each retirement account being divided. IRAs do not require a QDRO and are divided by divorce decree as a transfer incident to divorce.

How long does Illinois spousal maintenance last after a 20-year marriage?

Under 750 ILCS 5/504, Illinois courts may award indefinite maintenance for marriages of 20 years or longer. Indefinite maintenance terminates automatically upon the recipient’s remarriage, death, or cohabitation with a new partner on a continuing conjugal basis. The paying spouse may petition for modification based on a substantial change in financial circumstances.

What health insurance options does a spouse have after a gray divorce in Illinois?

An Illinois spouse losing employer health coverage through divorce has three options: federal COBRA continuation coverage for up to 36 months at up to 102% of the full premium; Illinois Spousal Continuation Coverage under 215 ILCS, which extends to Medicare eligibility for spouses age 55 or older; or an ACA Marketplace plan, which may carry premium tax credits for households below 400% of the federal poverty level.

Is spousal maintenance taxable in Illinois?

No. Illinois spousal maintenance awarded on or after January 1, 2019, is tax-neutral under current IRS rules — not deductible for the paying spouse and not taxable income for the receiving spouse. Maintenance orders finalized before January 1, 2019, follow prior tax rules under which payments were deductible for the payer and taxable income for the recipient.

What is the Illinois Spousal Continuation Coverage Law?

The Illinois Spousal Continuation Coverage Law (215 ILCS) requires all Illinois employers offering fully insured group health plans — regardless of employer size — to provide continuation health coverage to a spouse who loses group coverage due to divorce. For spouses age 55 or older at the qualifying event, coverage continues until Medicare eligibility at age 65. For spouses under age 55, coverage continues for up to two years.

What is a collaborative financial neutral, and why do gray divorce spouses need one?

A collaborative financial neutral is a Certified Divorce Financial Analyst who serves both spouses as a shared neutral professional in a collaborative divorce. In a gray divorce, the collaborative financial neutral models after-tax retirement income projections, long-term maintenance cost and duration, health insurance premium obligations through Medicare, and Social Security claiming strategies — so both spouses understand the verified financial consequences of every proposed settlement before signing.

Can a gray divorce spouse take immediate cash from a 401(k) through a QDRO without the 10% penalty?

Yes. A spouse receiving a QDRO distribution from a 401(k) can take an immediate cash distribution without incurring the 10% early withdrawal penalty — even if the receiving spouse is under age 59½. Federal ordinary income tax applies to the distributed amount. This penalty waiver applies only at the time of the initial QDRO distribution and does not apply to IRA divisions, which are governed by transfer-incident-to-divorce rules.

How does Social Security factor into a gray divorce settlement?

A divorced spouse married at least 10 years qualifies for Social Security spousal benefits equal to up to 50% of the higher earner’s primary insurance amount — without reducing the higher earner’s own benefit. The collaborative financial neutral models the optimal Social Security claiming age for both spouses, incorporating the resulting income projections into the full retirement financial picture.

Gray divorce demands financial precision. Anna K Law delivers it. Book a consultation to discuss your retirement assets, maintenance exposure, and health insurance options with Attorney Krolikowska and the collaborative team.

Anna P. Krolikowska, an attorney in the Northbrook law firm of Anna P. Krolikowska P.C, focuses her practice in the area of family law. Anna realizes that importance and the impact family law matters have not only on her clients, but also on their families. From divorce and child custody to any judgment modifications, Anna considers the unique circumstances of each case to develop a course of action designed specifically to address each client’s unique needs.